Beth Clewes discusses the impact of Covid-19, Brexit, energy prices and inflation on business confidence in the region. This blog post was produced for inclusion in the Birmingham Economic Review for 2022. The annual Birmingham Economic Review is produced by City-REDI at the University of Birmingham and the Greater Birmingham Chambers of Commerce. It is an in-depth exploration of the economy of England’s second city and a high-quality resource for informing research, policy and investment decisions. This post is featured in Chapter 1 of the Birmingham Economic Review for 2022, on the economy, crises and resilience. Read the Birmingham Economic Review. Visit the WMREDI Data Lab to find out more about Birmingham.

Business Confidence is the expectations that firms have for their future, often based on their current financial and operational conditions as reported through self-reported surveying. Data related to Business Confidence often fluctuates from quarter to quarter and is sensitive to regional and national political developments due to it being a reflection of where firms see themselves being in the next 12 months based on current economic conditions.

Measuring Business Confidence

At the Greater Birmingham Chambers of Commerce, Business Confidence is measured through our Quarterly Business Report survey, looking in particular at firms’ expectations around profitability and turnover for the following 12 months. The Quarterly Business Report is the most comprehensive survey of its kind in the city region, which shines a spotlight on indicators such as domestic and overseas sales, business confidence and recruitment and price trends.

Falling confidence

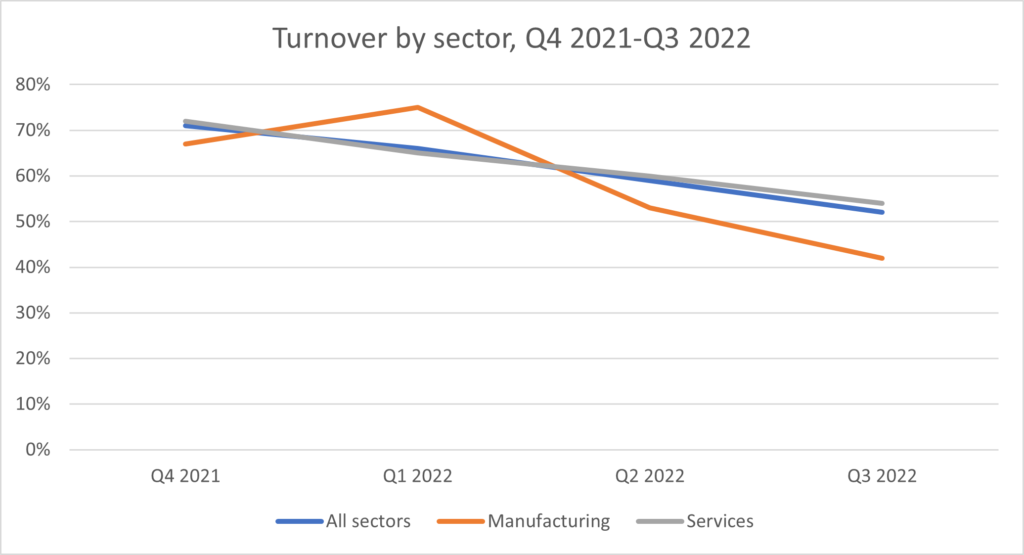

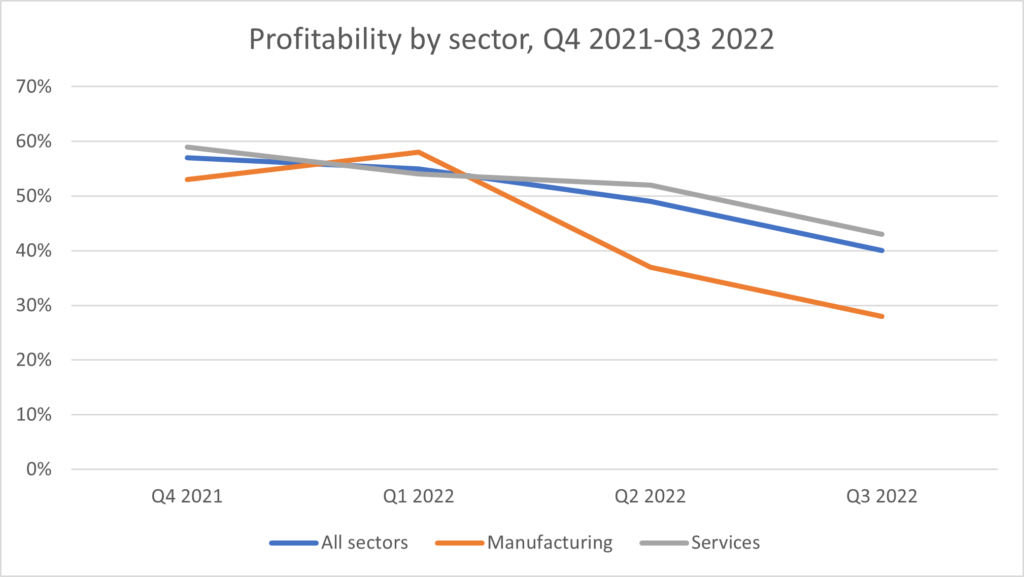

Over the past four quarters (Q4 2021- Q3 2022) the Greater Birmingham business community has seen a steady downturn in their turnover and profitability expectations, with manufacturers seeing more of a fluctuation than service firms for both measures.

As Figures 1 and 2 show, manufacturing firms experienced an increase in business confidence in Q1 2022, but then decreased again to below their service sector counterparts in the following quarter and have continued to decline. In contrast, service firms have seen a steady decrease in confidence in the past year.

Covid-19, Brexit, energy prices and inflation

As well as rising to the challenge of overcoming the twin headwinds of Covid-19 and Brexit recovery this year, firms are now facing a crisis around the cost of doing business, rising energy prices and record-high levels of inflation. It is perhaps no surprise that confidence has taken a hit when 55% of firms are expecting to increase their prices over the next three months. Energy prices are a major concern for employers at present- – of those businesses that are expecting to increase their prices over the next 3 months, 31% cited rising utility costs as the primary factor behind the decision. Anecdotally, as a result of the rising costs of doing business, service firms have had to pass down cost increases to customers, which will have a broader impact on levels of consumer spending – a key driver of economic growth in the UK. Concerns about inflation have also been growing over the past year, with a huge leap from being 19% of firms’ concerns in Q3 2021 to 40% in Q3 2022, the second-highest figure on record.

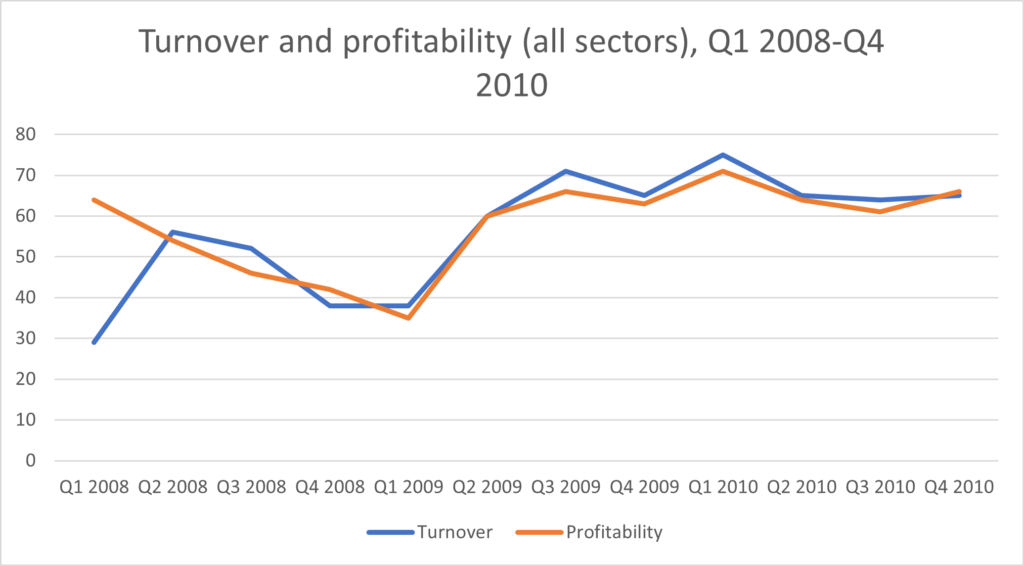

2008 Financial Crisis

While the most recent data may currently paint a sombre picture, the Greater Birmingham business community has overcome such challenges in the past, with the historical data from 2008 showing that the city region’s business confidence levels bounced back after the late-2000s recession.

The graph above shows that business confidence levels dropped when GDP began to fall in Q2 2008, prior to the technical onset of the recession (Q3 2008 was the second successive drop in GDP). At this point, the proportion of firms expecting an increase in profitability was at 54% and turnover at 56%. However, by the final quarter of the recession in Q2 2009, profitability projections were almost restored to their pre-recession level (with 63% of firms expecting it to increase) and the proportion of firms predicting an increase in turnover had doubled compared to Q1 of 2008 (to 60% of firms expecting an increase).

Optimism will rise again

The fact that Business Confidence measures rely on firms predicting a future that may not happen, especially during periods of turmoil where the future looks particularly unclear, means that the current figures reveal more about the sentiments that the business community are feeling right now, rather than evidence that conditions will be worse for firms in the next 12 months. While confidence has been impacted, we are optimistic that this will rise again as economic conditions improve and the scope of government support to get businesses through this period becomes clearer.

The Greater Birmingham Chambers of Commerce is on hand to help businesses in the local community to connect, support and grow through these challenges, and the Quarterly Business Report is one of the key mechanisms we use to inform ourselves of what is happening on-the ground. The sentiment we’ve gathered from local businesses over the past 25 years helps to direct our lobbying activity and gives us direction in terms of where to focus the support we offer as a Chamber.

You can read more about the Quarterly Business Report and access previous publications here.

This blog was written by Beth Clewes, Insight and Intelligence Services Manager, Greater Birmingham Chambers of Commerce.

Disclaimer:

The views expressed in this analysis post are those of the authors and not necessarily those of City-REDI, WMREDI or the University of Birmingham.