The Birmingham Economic Review is out now!

This year’s report will provide a comprehensive analysis of the city’s economy amid the wider geopolitical landscape, and actionable measures that businesses and stakeholders from across the city-region can take to drive economic growth.

Read the full Birmingham Economic Review 2025.

Huanjia Ma discusses how AI has become the buzzword of the year and is widely seen as a major opportunity for economic growth.

While the UK has early AI pioneers such as Google DeepMind, the domestic AI sector is not yet at the global frontier. Nevertheless, the opportunity is strong: the UK is estimated to have attracted over £20 billion in private AI investment between 2016 and 2024.

The Artificial Intelligence Sector Study 2024 estimates the UK’s AI ecosystem now includes more than 5,800 companies an 85% increase over two years generating £23.9 billion in revenue and contributing £11.8 billion in GVA. The AI Opportunities Action Plan argues for building a thriving domestic ecosystem serious players across the “AI stack” and widespread use of UK-made AI—so the UK is an “AI maker”, not an “AI taker.” The presence of AI firms (from foundational R&D to service providers) can boost regional growth by attracting high-skill, high-paying jobs and catalysing innovation spillovers.

A variety of AI firms presents in the economy. A Standard Industry Classification, which is commonly used to categories what a firm does, is not sufficient as it does not pick out a company focuses on the development AI, as they can locate in a wide range of industries. Some academic studies have looked at three layers of AI companies : base layer, technology layer and application layer. While DSIT adopts the following taxonomy of AI companies in their study in three layers:

- Dedicated vs diversified firms (who they are):

Dedicated AI firms make AI their main product or service. Diversified firms are broader businesses with a significant AI offering alongside other activities. - Business model (what they sell):

Builders of AI infrastructure (e.g., compute, platforms, tooling), AI product developers (software/models), and AI service providers (consulting, integration, managed services). (Note: users/adopters of others’ AI are out of scope here.) - Capabilities (what they can do):

Cross-cutting skills such as model development, computer vision, NLP, autonomy/agents, AI assurance/governance/safety, AI strategy & consulting, and AI skills & training. (Data mining is treated as part of other capabilities.)

Current AI business landscape in Greater Birmingham

According to Beauhurst Buzzword search, there are 180 AI firms headquartered in the Greater Birmingham, as of Setptember 2025, accounting for 1.8% of total UK AI firms, and account for 43% of AI firms in the West Midlands ITL1 region. London itself accounts for 5306 firms of the UK total. While Greater Birmingham trails behind more comparable LEP such as the Greater Manchester LEP, with 354 AI firms, it has shown acceleration speed.

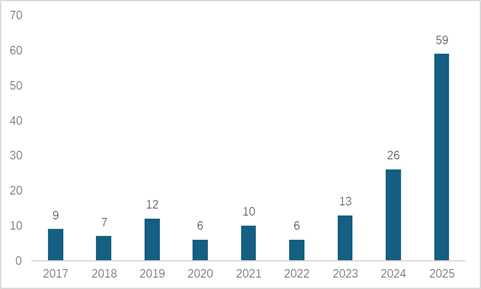

Figure 1 shows the total number of AI firms in the sector by year in the city-region. Overall, we have seen very positive growth in the number of new AI firms created. With only 9 months have passed in 2025, there are 59 AI firms established in the city-region, more than doubling the amount of new AI firms in 2024. This has shown very optimistic trajectory in the city-region to catch up.

Figure 1: AI companies’ creation in the Greater Birmingham city-region

Looking at which types of firms are there in the Greater Birmingham, developer of AI product and AI service providers seems dominate the playing field,

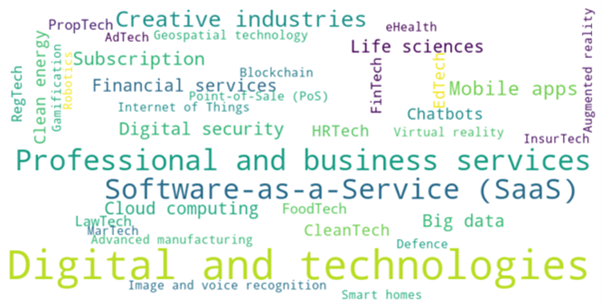

In the wordcloud (Figure 2) of Buzzword relating to AI firms, Professional and Business Services, as well as Software as Service, are among common things AI firms in the Greater Brimingham provides. For example, Capri Healthcare provides software for AI powered triage and referral management. Creative industries also plays an important role here, with over 12 AI firms in the city-region, focusing on AI powered marketing content such as Attentive Mobile.

Figure 2: Buzzword word cloud of AI companies in Greater Birmingham city-region

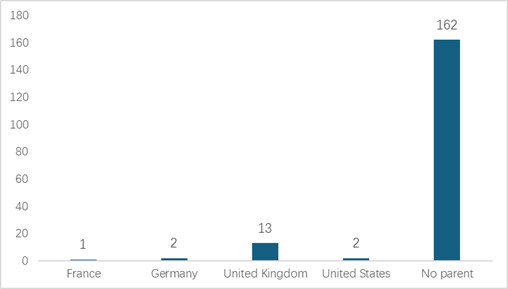

The majority of AI firms operate independently, with no parent company (shown in Figure 3). Of those who are subsidiaries, 5 are foreign owned, and 13 are domestic owned. This shows strong home-grown AI capabilities in the city-region.

Figure 3: Number of AI companies in the Greater Birmingham by the origin of ultimate parent company

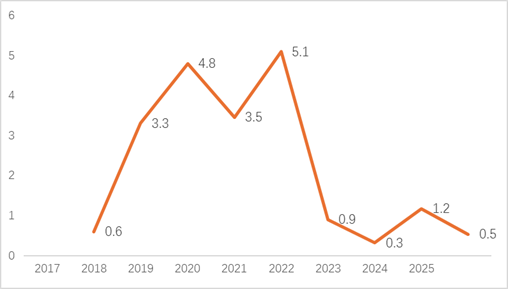

From 2017 to 2025 to date, AI firms in the city-region have totally raised over £20 million private through 22 deals, including private equity investments, angle investments and loans (showing in Figure 4). The peak of funding raises was from 2022 when £5.1 million was raised. While the last few years have seen relatively smaller funding raised, given the high number of AI firms created within the first three quarters of 2025, there is promising landscape in fundraising of AI firms in the city-region.

Figure 4: Fund raised (£m) of AI companies in the Greater Birmingham

Opportunities and Challenges co-exist

In summary, while Greater Birmingham City Region has not been in strong position comparative to London and South East in developing an AI sector, it has shown potential for developing a strong cluster, especially for firms in providing AI services and development of AI products. There are few obstacles need to be addressed:

Skills

West Midlands have stronger shortages in digital skills, compared to many other regions in the UK. But the city-region, and the West Midlands, has well placed infrastructure to address this. A cluster of high-quality tertiary education institutions producing well rounded graduates for the regional workforce ~ Warwick, Coventry and Birmingham and Aston Universities to name the key players.

Infrastructure

The UK had ~1.6 GW of total data centre power capacity (all-purpose) in 2024. Many of these data centres are clustered in Greater London, making London one of Europe’s largest data centre markets. New hubs are emerging in Manchester and South Wales. This puts the West Midlands, and the city-region, into less advantageous position. But there comes to opportunities. Because many existing data centres are optimized for general enterprise workloads rather than high-density AI computing, their architecture and energy systems may make them less suitable for AI without upgrades. While new data centres that are purposefully built for AI creates a gap allowing for stronger growth.

Funding

Financial constraint faced by AI startups in the UK is named one of the biggest obstacle for AI companies to scale up.

Investments into AI companies in the city-region require a major boost according to the data. According to the UKRI WAI finder database, West Midlands only hosts 12 of 508 AI related Incubator/accelerator, accounting for 2.3%. This trails behind comparable regions of Northwest, hosting 31 AI-related Incubator/accelerator, and East Midlands, which has 15 AI-related Incubator/accelerator.

This blog was written by Huanjia Ma, Research Fellow at City-REDI, University of Birmingham.

Disclaimer:

The views expressed in this analysis post are those of the author and not necessarily those of City-REDI or the University of Birmingham.