Rebecca Riley discusses a new report examining productivity in the West Midlands. The report is written by Melisa Wickham and is in collaboration with the West Midlands Combined Authority.

This report focuses on labour productivity – which measures how much output is produced per unit of labour input. There are varying measures of labour input, determined by data availability.

Measuring Output

Ideally, the measure should reflect what actually goes into the production process – it should be based on actual hours worked and quality-adjusted (for skills, education, experience levels etc.). Readily available estimates are often not produced to this ideal. The labour productivity data used are not quality adjusted and use a mix of hours and more simple measures of per worker or per filled job. In reality, using hours or workers as the productivity denominator often makes little difference to the growth in productivity observed or the relative productivity picture across the UK.

Measures of regional output, which form regional productivity estimates, include an element of modelling (to apportion firm-wide output to local plants and proxy missing data) and this can underestimate the true output generated in regions outside of London whilst overestimating the value of output in the Capital, due to issues such as where headquarters are registered.

More broadly, and an issue that applies to all output estimates (including at national level), there is a question as to how well national accounts incorporate intangible capital (data, branding and so on). This can lead to underestimates of the true value of output and is likely to be more important for certain sectors (as they are often knowledge-based assets, they are likely to be more important in knowledge-based sectors).

What is meant by Growth?

Growth in productivity means an economy can produce more without needing to use more inputs. As such, it is one of the most fundamental drivers of improvements in living standards, allowing people to enjoy more, or better quality, goods and services.

At the national level, capital shallowing (workers having less capital per hour worked) and slower growth in multi-factor productivity (which can be driven by technological progress, economies of scale, improved management or business processes or efficient use of inputs) has been a drag on labour productivity growth (output per hour worked) since the 2008 economic downturn.

The former, accounting for around a third of the productivity gap, is likely the result of business uncertainty driving a reluctance to invest in capital, which is often the less flexible input to production (compared to labour). In contrast, labour composition (or the quality of labour) has maintained its pre-downturn trend and helped to mitigate the extent of the productivity gap with the pre-downturn trend.

Data

The output data used in the ONS regional firm-level productivity analysis is derived from the Annual Business Survey (ABS). This includes all local units (for example each office, factory, warehouse etc) of a firm registered on the Inter-Departmental Business Register (IDBR). Local units of a firm/enterprise may be engaged in different parts of the business such as production, accounting or head office. Therefore, each local unit is assigned its own Standard Industrial Classification 2007 (SIC 2007) code, which corresponds to the local unit’s principal activity. However, the allocation of business activities in firms with multiple local units is likely to underestimate the value that is attributable to some areas and the data is not adjusted for price variations across regions.

The ABS excludes the agricultural and financial sectors as well as some small firms, the self-employed and the public sector. As such, the analysis covers approximately two-thirds of the UK economy in terms of gross value added.

In most cases, local plants, reporting units and enterprises are one and the same. On average, around one-quarter of the local plants across regions belonged to a multi-plant enterprise in 2015, with the North East having the highest (31%) and London having the lowest (21%) proportions. The larger the enterprise, the more likely they are to have more than one plant. In the dataset, over 95% of the enterprises with 250 or more employees were multi-plant enterprises and over 90% of the micro-plants were single establishments across the regions and countries in Great Britain.

As discussed, productivity data has limitations and is far from perfect, but this report looks to unpick the productivity issues in the region using the information we have available to date. This should be treated with caution but still enables us to shed light on the issues. The West Midlands has one of the largest inter-regional gaps in productivity, and any growth has been unevenly spread. The areas with the highest productivity in 2004 had the greatest growth, which suggests long term path-dependency.

Key findings of the report:

- The ONS estimates the average market sector wage in the UK would be just over £5,000 higher in 2018 for the average worker if productivity growth had continued.

- Productivity gaps across countries and within regions are not uncommon, but the variation within the UK is high compared to international standards. In the West Midlands GOR, labour productivity was 11% below the UK in 2019, and 33% lower than the most productive region (London).

- If the West Midlands had the same industrial structure as Great Britain (but retained its average productivity for each industry) it would have an 11-percentage point gap in productivity with the GB average (firm productivity index). In contrast, if it retained its industrial structure but each industry had the same productivity as GB the productivity gap would only be 1 percentage point.

- In West Midlands the industry mix effect is positive (+3-percentage points) but not large enough to offset the firm productivity effect (-11-percentage points).

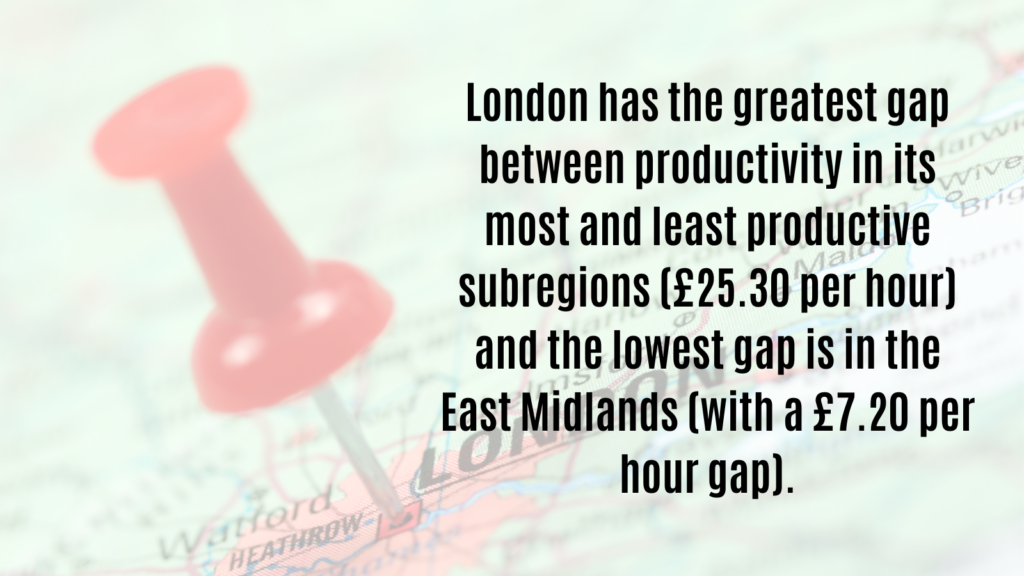

- Only 3 subregions in the wider West Midlands had labour productivity levels above the UK average in 2019 (even when London is excluded from the average); Solihill was the highest (£45.20 per hour), followed by Warwickshire (£37.40 per hour) and Coventry (£36.20 per hour).

- Hertfordshire, Worcestershire & Warwickshire are some of a handful of places where the industry structure has a more significant effect on aggregate productivity than firm-level productivity. And both the industry structure and plant productivity have a positive effect on relative productivity.

- Local plant productivity in the West Midlands’ Less Knowledge Intensive Services (LKIS) is the most widely spread. And median productivity in these sectors (£25,110 per worker) is more than half that in the Knowledge Intensive Services (KIS, £55,430) and Medium/High Tech Manufacturing (MHTM, £57,190).

- Given the size of the Less Knowledge Intensive Sector (making up over half of the local plants in the West Midlands and accounting for nearly 60% of employment) it is important in explaining the aggregate productivity gap.

- Local plant productivity in the West Midlands’ Less Knowledge Intensive Services is the most widely spread; those in the top 75% are 3.2 times more productive than those in the bottom 25%. Meanwhile, the spread of plant productivity in Knowledge Intensive and Manufacturing sectors is very low.

- The high median productivity of micro firms can be partly explained by their higher share in the more productive KIS industries. In the West Midlands, whilst 76% of all local plants were micro firms this proportion rises to 89% and 87% within KIS and ‘Other’ sectors respectively.

- The West Midlands has a high share of plants in the LKIS within the top 20% of the productivity distribution. With nearly one in every 2 plants in the top 20% (48%) the share is over 4 times larger than in London (11%) and 9 percentage points above the second highest region (North East).

- London and the South East, which have productivity above the UK average, have the top 20% of the productivity distribution dominated by plants in the KIS.

- For the West Midlands, the gap is high – it is the 4th highest region in absolute difference and 2nd in percentage difference.

- There is a narrow spread of plant productivity within both the medium-high and low-medium manufacturing sectors in the West Midlands which may reflect a narrow range of activity within these broad sector classifications.

- Plants in the ‘other’ sector (composed of primary and utilities, real estate and construction) play a significant role in the upper quintile of the productivity distribution in the West Midlands (40%), despite making up only one in six (16%) of all plants in the region.

- The impact of age and size may simply be attributable to their dominance in certain industries – plants of larger and older firms may be more prevalent in naturally more productive sectors.

- Micro firms (with 1-9 employment) have the highest median productivity and are most concentrated in the more productive KIS and ‘other’ sectors. Consequently, they have a higher representation in the upper quintile of the productivity distribution. However, plants of larger firms have higher average productivity driven by a long top tail.

The Differences

In the non-financial business economy, differences within industries explain more of the UK regional productivity gaps. Some of this may be due to regional price differentials that are not picked up in the data, particularly in the non-tradeable goods/services.

Some may also be the result of the data not being quality adjusted (so not accounting for occupational/skill composition) within the same industry across regions or due to other differences hidden in the sector classifications. For example, a multinational law firm in London may have a different specialisation (hence different labour productivity levels) to a small local law firm elsewhere, but both will have the same two-digit industry grouping.

Firm productivity differences can also be driven by a myriad of internal (age, size, management, foreign investment) and external (infrastructure, agglomeration, market size etc) factors. Further research may be needed to hone in on how these affect the firm-productivity within the West Midlands specifically.

Analysis

The analysis shows that in general there are little variations in productivity by age and size and the underlying issue is the distribution of companies in knowledge-intensive industries.

Older firms also have a higher representation of plants in the bottom 20% of the productivity distribution, meaning some of the least productive plants tended to be part of older firms. On the other hand, there is a higher representation of young firms (<6 years) in the top 20% of the productivity distribution.

However, whilst productivity growth drives growth in incomes it does not necessarily drive wellbeing. London, for example, has the highest productivity in the UK but scores lowest on life satisfaction and worthwhileness measures1. This is important to bear in mind – improving productivity may mean households are financially better off but it doesn’t automatically follow that their wellbeing is higher.

This blog is also part of the Productivity in the West Midlands project by WMREDI. You can find out more here.

This blog was written by Rebecca Riley, City-REDI / WMREDI, University of Birmingham.

Disclaimer:

The views expressed in this analysis post are those of the authors and not necessarily those of City-REDI, WMREDI or the University of Birmingham.