Alice Pugh looks at the impact of the Autumn Budget on households, businesses and public services. View Alice’s previous blog on this topic – Key Announcements Autumn Statement 2023 Household Impact The Institute for Fiscal Studies (IFS) has found that the changes to National Insurance Contributions (NICs) for employees and the self-employed, will only give … Continue reading “The Autumn Statement 2023: The Impacts”

Tag: Autumn Statement

Trick or treat? What will probably be in the 2018 Budget – and what ought to be

Find out what was accurate about this forecast – and what wasn’t – by tuning into Radio 4’s Today programme on Monday morning. City-REDI’s Professor Simon Collinson will be one of the guests, discussing the budget and what it means for the country in what promises to be a tumultuous year ahead. There’s been plenty … Continue reading “Trick or treat? What will probably be in the 2018 Budget – and what ought to be”

#Budget2017 – Sailing the ship in troubling times

This year’s autumn statement paints a dramatic statement for growth prospects, with the growth forecast for 2017 downgraded from 2% to 1.5% and GDP falling further to 1.4%, 1.3% and not rising until 2020. Business investment has been revised down and CPI forecasts it to fall later this year. £3bn has been set aside to … Continue reading “#Budget2017 – Sailing the ship in troubling times”

After the Autumn Statement, winter is coming?

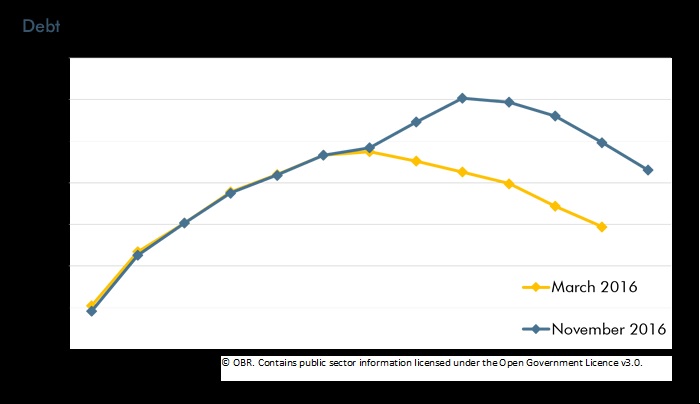

This year’s Autumn Statement paints a dramatic statement for prospects for growth. Instead of being in the black we are now in the red. Borrowing is back, and public spending restraint is a bit looser, but are the measures in the Autumn Statement going to drive growth and help those most affected by austerity? Although … Continue reading “After the Autumn Statement, winter is coming?”

All Change? The New Politics of Austere Ambition

Following his predictions of the Autumn Statement earlier this week (which can be found here), here City-REDI’s Prof. John Bryson reflects on yesterday’s announcement. “Yesterday’s Autumn Statement reflects a somewhat limited ambition that is constrained by the UK’s structural deficit. There are rather too many uncertainties related to Brexit, the continued underlying weakness of the European … Continue reading “All Change? The New Politics of Austere Ambition”

Mayflation, Hammflation or Trumpflation?

Here, City-REDI’s Prof. John Bryson shares his predictions ahead of today’s Autumn Statement when Chancellor Philip Hammond will outline his plans for UK taxing and spending. This will be the Chancellor’s first major economic statement since the UK voted to leave the EU in June. “On Wednesday 23 November, a very different style of Autumn Statement will be … Continue reading “Mayflation, Hammflation or Trumpflation?”