Like any good Hollywood blockbuster you can think of, here we finish the trilogy of blogs related to the economic exposure to COVID-19 of the West Midlands’ sectors [1]. If you are still reading this series and you are not overwhelmed yet by the amount of information (and disinformation) related to the pandemic, I hope you like this last part. You can read the first blog here, where I examined how dependent the West Midlands economy is to foreign trade, where it originates and it’s outward destinations. Part two looked at sectoral linkages of human health activities in our region and the estimation of the indirect workers, often forgotten and always invisible to anyone demanding health services. You can read the second blog here.

To conclude, I will try to approximate the effects of a lockdown in the regional economy. Let’s start by saying that any simulation of this scenario is highly unlikely to be accurate [2] because there is a high level of uncertainty concerning the behaviour of any agent in the system (consumption by the households, government financial injections, imports and aid from other regions/countries, etc.). As I mentioned already at the beginning of this series, no model has been developed for addressing big shocks like the one we are going to suffer in the coming months (both during and after the lockdown). However, it is still better to try and have some indications based on pre-shock production structures than to guess these effects blindfolded.

On the 24th of March, we officially entered into lockdown in the UK. What was a suggestion has now become an imposition, and from today, police will be authorised to make people stay home. From the experience in other European countries, which have been in lockdown for some time now, we can see that this situation has clear economic effects. Some particular sectors will be forced to close in order to avoid gatherings and social interaction. Those are mainly accommodation and food service activities (restaurants, bars, hotels, etc.) and arts, entertainment and recreational activities (museums, sporting events, etc.). On a second level, some sectors are going to see how their demand is reduced due to the number of people working from home [3]: rail transport and transport services, personal services and business activities in general. Basic sectors will see their demand increased for some months: Electricity and energy, water supply, retail trade, information and communication, scientific and technical activities, and of course, human health services.

Table 1 summarises the unbelievable amount of different shocks that could happen by sector.

Table 1. Lockdown scenario by sectors.

| SIC Code | Sector | During the lockdown | Simulation |

| A | Agriculture, forestry and fishing | Not specified | – |

| B | Mining and quarrying | Not specified | – |

| CA | Manufacture of food, beverages and tobacco | Not specified | – |

| CB | Manufacture of textiles, wearing apparel and leather | Not specified | – |

| CC | Manufacture of wood and paper products and printing | Not specified | – |

| CD-CF | Manufacture of petroleum, chemicals and pharmaceuticals | Not specified | – |

| CG | Manufacture of rubber, plastic and non-metallic minerals | Not specified | – |

| CH | Manufacture of basic and fabricated metal products | Not specified | – |

| CI | Manufacture of computer, electronic and optical products | Not specified | – |

| CJ | Manufacture of electrical equipment | Not specified | – |

| CK | Manufacture of machinery and equipment | Not specified | – |

| CL | Manufacture of transport equipment | Not specified | – |

| CM | Other manufacturing, repair and installation | Not specified | – |

| D | Electricity, gas, steam and air-conditioning supply | Open as a basic sector | Increase demand by 25% in a quarter |

| E | Water supply; sewerage and waste management | Open as a basic sector | Increase demand by 25% in a quarter |

| F | Construction | Not specified | – |

| G | Wholesale and retail trade; repair of motor vehicles | Open as a basic sector | Increase demand by 25% in a quarter |

| H | Transportation and storage | Reduced demand | Decrease demand by 25% in a quarter |

| H_rail | Rail transport services | Reduced demand | Decrease demand by 75% in a quarter |

| I | Accommodation and food service activities | Closed | No production and no demand for a quarter |

| J | Information and communication | Working remotely (from home) | Increase demand by 25% in a quarter |

| K | Financial and insurance activities | Working remotely (from home) | Decrease demand by 25% in a quarter |

| L | Real estate activities | Working remotely (from home) | Decrease demand by 25% in a quarter |

| M | Professional, scientific and technical activities | Working remotely (from home) | Increase demand by 25% in a quarter |

| N | Administrative and support service activities | Working remotely (from home) | Decrease demand by 25% in a quarter |

| O | Public administration and defence; compulsory social security | Working remotely (from home) | Decrease demand by 25% in a quarter |

| P | Education | Working remotely (from home) | Decrease demand by 25% in a quarter |

| Q | Human health and social work activities | Open as a basic sector | Increase demand by 25% in a quarter |

| R | Arts, entertainment and recreation | Closed | No production and no demand for a quarter |

| S | Other service activities | Working remotely (from home) | Decrease demand by 75% in a quarter |

| T | Activities of households | Closed | No production and no demand for a quarter |

This extreme scenario is quite rough because there is not much data to work with from any source in order to design more realistic demand increases/decreases at the moment. Some of the services are closed until further notice, and the length of this crisis cannot be predicted either. We will look at a quarter of a year (whole spring, i.e. Q2) since it took 2 months for the first country affected to relax some of the lockdown measures. To see the exposure of the sectors to the lockdown, I am going to use the SEIM-UK [4] Input-Output framework and both demand shocks and the Hypothetical Extraction Method. [5]

In table 2 you can see the results of shutting down the accommodation and food services, as well as arts, entertainment, sports and recreation sectors for 3 months. The number of jobs at risk, directly and indirectly, are close to 61,000; 27,000 are directly related to the hospitality services and 7,000 to the recreational activities. Two of the main three sectors of the region in terms of employees (professional, scientific and technical activities; and wholesale and retail trade) will be affected too (around 8,000 and 5,000 indirect jobs, respectively) [6]. The figures shown for the output and the GVA corresponds to annual values, not quarterly results. It means that in Q1, Q3 and Q4 the economy would function as usual, while the shock only affects Q2. However, even under this assumption, the negative impact in Q2 would mean a 3.5% reduction in the GVA of the whole year.

Table 2. Closure of Accommodation and food service activities (SIC – I) and Arts, entertainment and recreation (SIC – R) for 3 months. Annual figures.

| Variable | Value | % |

| Output | -3.48% | |

| Gross Value Added | -3.54% | |

| Employment | -5.00% | |

| Number of Jobs | -61,085 | |

In table 3, we see services that will be used less while people work from home, like transportation services, with demand being reduced by 25% during the second quarter of the year. As expected, the negative effects are higher than in the previous simulation: 86,000 jobs at risk, meaning the 7.1% of the employment in the region. Education, the fourth most important sector in the West Midlands economy in terms of employment appears as highly affected, with 8,000 jobs exposed to the lockdown.

Table 3. The scenario in table 2 + Reducing the demand for services sectors due to working from home for 3 months. Annual figures.

| Variable | Value | % |

| Output | -5.70% | |

| Gross Value Added | -6.06% | |

| Employment | -7.07% | |

| Number of Jobs | -86,308 | |

Finally, in table 4, we include the increase in the demand for basic sectors. As we have been witnessing these last weeks, our consumption behaviour has changed and, as we spend more time at home, we are using more electricity and water than before. The same thing is happening with communication and information given the extraordinary use of the internet and video calls at the moment. Sectors like human health (as discussed in the second blog) and wholesale and retail trade are the most obvious ones seeing their demand increase, together with shortages and capacity constraints.

In this case, the negative results of the previous table are partially compensated by the increased demand in other services, setting the number of jobs at risk in the West Midlands economy at around 65,000.

Table 4. The scenario in table 3 + Increasing the demand for basic sectors for 3 months. Total results. Annual figures.

| Variable | Value | % |

| Output | -4.40% | |

| Gross Value Added | -4.75% | |

| Employment | -5.31% | |

| Number of Jobs | -64,806 | |

Table 2, 3 and 4 present the main results obtained from this 3-month scenario step by step [7]. Summarizing, in the first step (Table 2), we calculated the effect of closing restaurants, bars, hotels and leisure activities. This alone will represent the main negative impact on the economy, with slightly more than 61,000 jobs at risk directly and indirectly. Step 2 (Table 3) includes the reduced demand that some sectors would experience in the case of a lockdown. The GVA would drop from -3.5% to -6.0%. Finally, if we include some of the potential increases in demand for some basic sectors, the negative impact would be moderated to a -4.7% loss in the GVA for the year 2020.

Again, these figures do not take into account the supply constraints associated to each sector, possible price and wage effects, types of contracts, or the more than likely ‘V’ shape that the economy would reflect in the 3rd quarter (assuming the lockdown would last for up to 3 months). According to JP Morgan estimates, the real GDP of the UK economy is forecasted to be reduced in the first quarter by -10% and by -30% in the second quarter. A sharp increase of 50% is projected for the third quarter (showing the ‘V’ shape mentioned before, normal in a disaster situation). In the entire year, the whole economy would show a negative -0.8% GDP growth, according to their estimations. All of this goes without taking into account the potential effect that this crisis can have in the decision-making process and the behaviour of households afterwards.

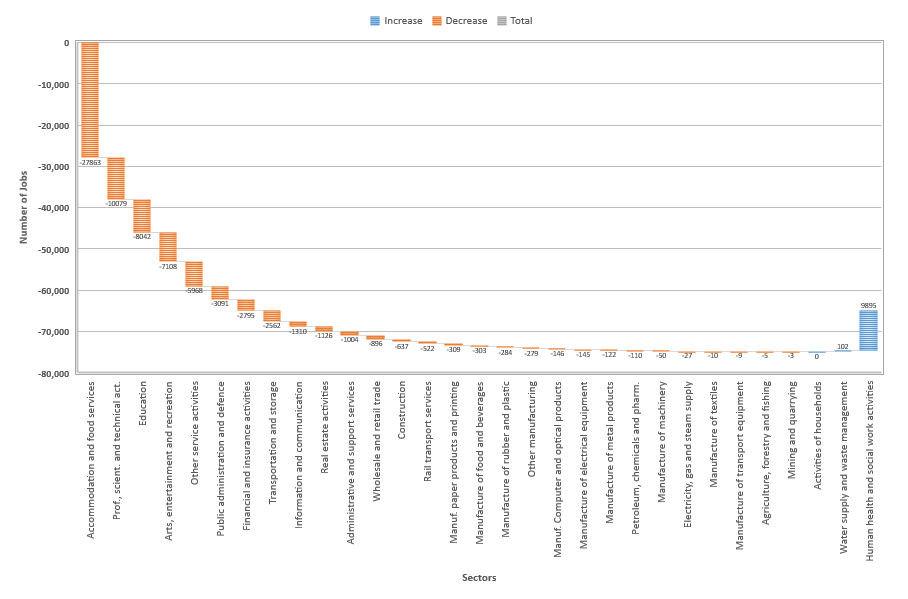

The main sectors affected by the lockdown scenario (as described in Table 1) are shown in Figure 1. As expected they would be accommodation and food services and recreational activities, which had to close completely (and cannot provide their services from home) [8]. However, other sectors linked indirectly would see their number of employees being at risk: professional and technical activities, education, other personal services or transportation, for example. Mainly services. The positive sign [9] comes from the Health Service sector, which would need an extra 10,000 workers to meet a 25% increase in its demand in the following 3 months (assuming the productivity of the workers remain the same) [10].

Figure 1. 3-month Lockdown economic impact by sectors in terms of employment.

We should not forget that there is no economy without people, and the welfare of people is at the heart of the economy. Extreme situations require exceptional measures, and it is up to the government to make the right decisions to mitigate the crisis and alleviate the economic costs of it, without losing people on the way. This situation will end at some point and it is better to try to come out of it without regretting any decision made (or not made).

As a final point, a friendly piece of advice. Stay at home and be careful if you go out for exercise. Please think about how you can help during this period of lockdown, too. We can all do something. Even small contributions could make a great impact.

Footnotes

[1] In this piece, when we refer to the West Midlands Economy we are considering the NUTS2 classification (UKG3) that includes Birmingham, Solihull, Coventry, Dudley, Sandwell, Walsall and Wolverhampton regions. An area with a population estimated of 2,916,458 inhabitants (2018) and that corresponds to the West Midlands metropolitan county.

[2] Another disclaimer is that, in the actual version of the SEIM-UK model, there is no specification of supply constraints, which would be very much needed in a scenario like the one proposed to see possible bottlenecks in the production process.

[3] In this case, I will just refer to consumption (private and public).

[4] The SEIM-UK model is a Multiregional Input-Output model for the UK with 2016 as the base year developed at City-REDI Institute of the University of Birmingham. Find out more here.

[5] See Dietzenbacher, E., Linden, J. A. V. D., & Steenge, A. E. (1993). The regional extraction method: EC input-output comparisons. Economic Systems Research, 5(2), 185-206. See also Dietzenbacher, E., van Burken, B., & Kondo, Y. (2019). Hypothetical extractions from a global perspective. Economic Systems Research, 31(4), 505-519.

[6] As I explained before. This is accounting for the number of jobs exposed, it doesn’t mean that it is the number of people losing their jobs by any means. Wages in all sectors are going to be affected or negotiated. For example, in sports activities, some teams are negotiating a salary reduction with their players during this period, which may help to mitigate exposure and reduce job losses at their clubs.

[7] Take these figures very carefully. The most interesting result of this exercise that there are indirect effects and what sectors these impact upon.

[8] Although food delivery could be an exception.

[9] Unless isn’t enough human health specialists in the region available to meet this demand.

[10] The increase in demand can be higher than this 25%. It will all depend on the shape of the curve of cases related to COVID-19.

This blog was written by Andre Carrascal Incera, Research Fellow, City-REDI.

Disclaimer:

The views expressed in this analysis post are those of the authors and not necessarily those of City-REDI or the University of Birmingham

To sign up for our blog mailing list, please click here.

3 thoughts on “Economic Exposure to COVID-19 (Part III): The Situation in the West Midlands Region – The Sectoral Effects of a Lockdown”